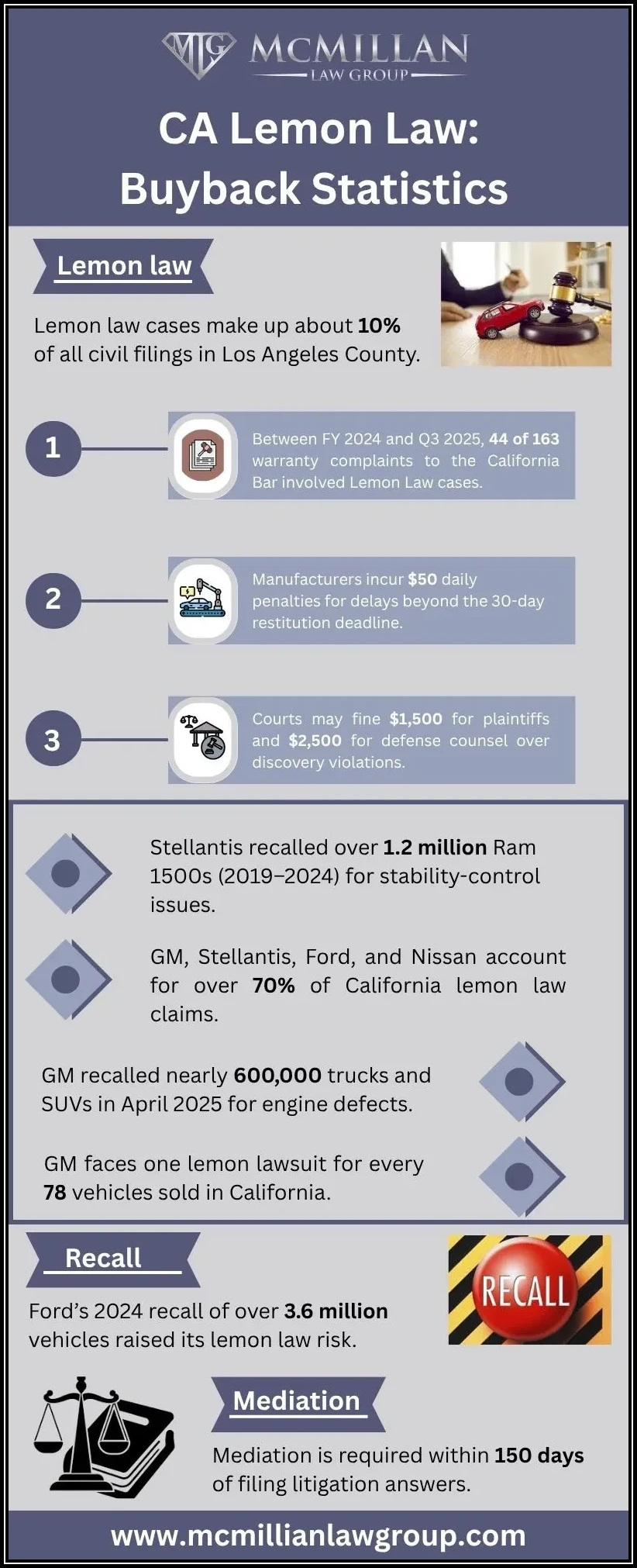

California’s Lemon Law, also known as the Song-Beverly Consumer Warranty Act, provides robust safeguards for consumers dealing with faulty vehicles, including the possibility of buybacks or replacements. Nevertheless, for individuals who have financed their vehicles, it is essential to grasp how outstanding loan balances can influence Lemon Law claims in order to secure a just resolution.

Understanding the Basics of California Lemon Law

Grasping the Fundamentals of California Lemon Law

California’s Lemon Law is designed to safeguard consumers who buy or lease new vehicles, and in some cases used ones, that exhibit significant defects and remain unfixable after a reasonable number of repair attempts. If a vehicle fits these criteria, it is labeled a “lemon.”

Responsibilities of the Manufacturer: Replacement or Buyback

When a vehicle is deemed a lemon, the manufacturer is obligated to either replace it or buy it back. The buyback process entails reimbursing the consumer for the initial down payment, ongoing monthly payments, registration fees, and settling the remaining loan balance, with a deduction for the mileage accrued prior to the defect being reported.

What Is a Loan Balance in Lemon Law Cases?

The amount remaining on the vehicle financing agreement at the time of a Lemon Law settlement is referred to as the loan balance. In California, many buyers choose to finance their vehicles instead of paying for them in full. When a manufacturer consents to repurchase the vehicle, the critical issue is determining how much of the remaining loan balance they will settle.

According to California regulations, manufacturers are generally required to pay off the unpaid loan balance during the Lemon Law buyback procedure. Nevertheless, various financial elements can lead to potential complexities in this process.

- The initial purchase price and overall loan amount

- The interest rate applied to the loan

- The number of payments that have been made by the consumer

- Whether the buyer had previously traded in another vehicle and included that loan in the new one.

- Any late fees or penalties incurred.

- Negative equity from a previous loan

Negative Equity: A Hidden Pitfall

A significant challenge arises from negative equity, which happens when a buyer exchanges a vehicle that has a lower value than the outstanding loan amount. This negative equity is frequently added to the new loan for the vehicle being purchased.

To illustrate:

- Vehicle A is traded in for $10,000.

- The outstanding loan on Vehicle A is $15,000.

- The $5,000 difference is incorporated into the loan for Vehicle B (the new purchase).

As a result, the loan for Vehicle B not only covers its purchase price but also includes the additional $5,000 of negative equity carried over from Vehicle A. If Vehicle B proves to be defective, the manufacturer is only responsible for the value of Vehicle B itself and not for the leftover debt associated with Vehicle A.

This creates a gap in the loan balance, which means the consumer might still be liable for paying off the remaining debt that isn’t linked to the faulty vehicle.

Usage Deduction and Its Impact on Loan Balance

One of the factors that affects the outcome of loan balances is the deduction for usage. This deduction reflects the number of miles driven before the defect in the vehicle was initially reported, and it decreases the total amount that the manufacturer is obligated to refund.

In California, the usage deduction is calculated using the following formula:

(Mileage at the time of the first attempt to repair) ÷ 120,000 × Purchase Price

For instance, if a vehicle was purchased for $30,000 and the defect was reported when it had traveled 6,000 miles, the calculation would be:

6,000 ÷ 120,000 × $30,000 = $1,500 usage deduction

This deduction can influence whether the repurchase amount will be enough to cover the entire loan balance. If the loan amount is substantial and the usage deduction is considerable, the consumer might find themselves with an outstanding loan balance—something a qualified California Lemon Law attorney can help you navigate and resolve.

Lease Buybacks and Loan Balance

Although leases are distinct from conventional loans, they come with financial responsibilities akin to those found in loans. Lease buybacks also present unique difficulties. Typically, in a lease agreement, the manufacturer will reimburse the following:

- Total lease payments already made

- The initial down payment

- Outstanding lease payments

- Fees for disposition and registration

Nonetheless, if the leasing agreement encompasses additional features, aftermarket items, or penalties for early termination, the leasing company may not always eliminate these charges, potentially leaving consumers with costs they still have to address.

Manufacturer Disputes and Incomplete Payoffs

Frequent Conflicts Regarding Loan Amounts

Manufacturers might dispute particular elements of a consumer’s loan amount during a Lemon Law buyback process. Issues often surface related to high interest rates or financing obtained through unconventional lenders. These disputed factors can considerably decrease the repayment amount that the manufacturer is prepared to offer.

Exclusions for Additional Products

Products that are not directly associated with the vehicle, like GAP insurance, extended warranties, or service contracts, are commonly left out of reimbursements from manufacturers. Consequently, consumers may need to engage in negotiations for partial repayments, complicating the financial settlement process.

How a California Lemon Law Attorney Can Help

Addressing challenges related to loan balances necessitates expertise in legal and financial negotiations. An experienced California Lemon Law lawyer can:

- Review the loan documents to pinpoint all outstanding amounts.

- Engage with the manufacturer to negotiate buyback conditions that guarantee just compensation.

- Explain issues related to negative equity and work to transfer liability.

- Verify that the deduction for usage is computed correctly.

- Assist the consumer in grasping any remaining financial responsibilities after the settlement.

In the absence of legal advice, consumers might inadvertently accept a settlement that fails to address the full amount of their loan, resulting in continued debt responsibilities even after they return the defective product.

Problems related to loan balances, including negative equity, deductions for usage, and disputes over add-on products, can impact the amount you receive in a California Lemon Law case, potentially resulting in unanticipated expenses. To safeguard your rights and enhance your potential compensation, it’s essential to seek advice from an experienced San Diego Lemon Law lawyer if you have financed a faulty vehicle.