Understanding Lemon Law Buybacks and How Loan Balances Fit In

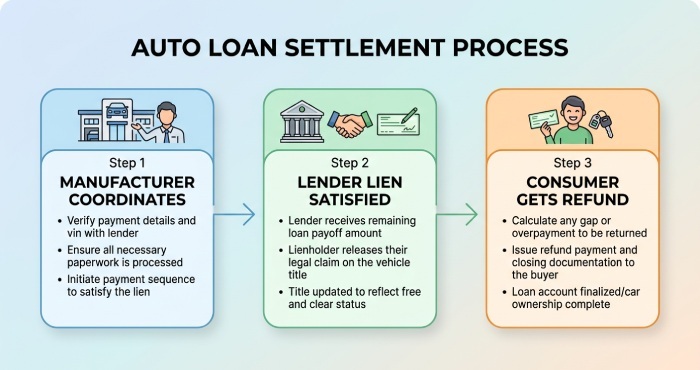

A lemon law settlement involving a financed vehicle is more than a simple cash payment. When a manufacturer agrees to a buyback, it must first address the outstanding car loan by coordinating with the lender. Only after the loan payoff is calculated can any remaining refund be paid directly to the consumer.

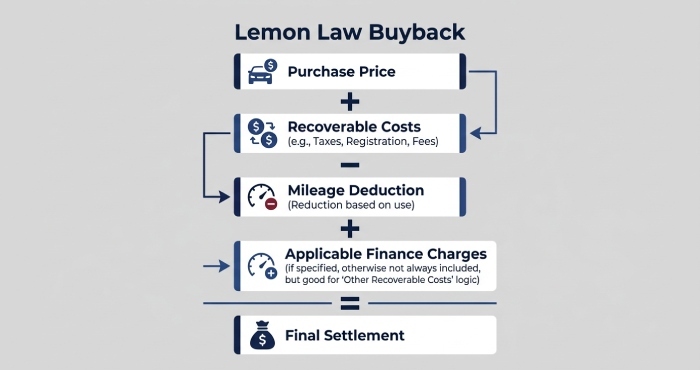

In a typical lemon law claim, the buyback amount may include the purchase price or eligible payments made by the consumer, less any lawful mileage deduction and plus certain recoverable costs. The manufacturer works with the bank or finance company to obtain the current payoff amount before completing the settlement.

Because the lender holds a lien on the vehicle, the loan must generally be satisfied before ownership can be transferred back to the manufacturer. Reviewing the payoff amount, accrued interest, and any remaining loan balance is an important step, and a lemon law attorney can help ensure the settlement is calculated correctly.

What Happens to Principal vs. Interest in a Lemon Law Settlement

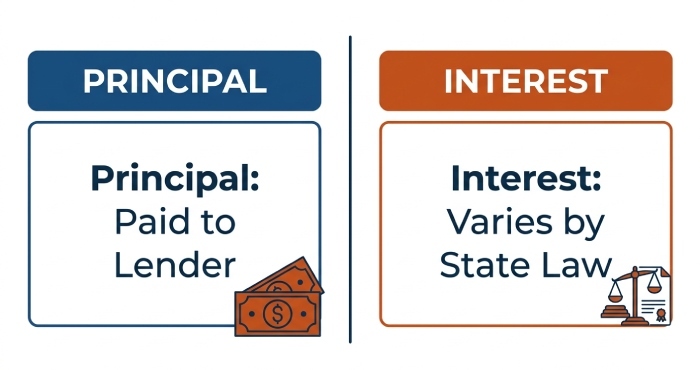

The principal on a car loan is the amount borrowed to purchase the vehicle, while interest is the cost of borrowing that money. In a lemon law settlement, the loan principal is usually resolved through the lender payoff so the loan can be satisfied and the vehicle title transferred.

Whether a consumer can recover interest already paid depends on the applicable state law and the terms of the settlement. Under the California Lemon Law, many purchase-related payments may be recoverable, but finance charges are not always reimbursed and may be treated differently depending on the loan agreement and the specific facts of the case.

Principal Usually Follows the Payoff

The remaining loan principal is usually shown on the payoff statement. If the buyback exceeds the payoff amount, the consumer may receive the remaining balance as a refund.

Interest Is Reviewed Differently from Principal

Loan interest is not always treated the same as principal in a buyback. Whether it is reimbursed depends on the settlement terms and the specific case.

Review the Retail Installment Contract

The retail installment contract outlines the loan details, finance charges, and any add-on products. Reviewing it helps identify costs included in the vehicle financing.

Compare Payment History to Payoff

Your payment history shows how much was applied to principal and interest over time. Comparing it with the final payoff helps verify that the settlement is accurate.

When Interest Paid May Be Reimbursed or Excluded

Interest paid on a loan for a defective vehicle may be recoverable if it is directly tied to the consumer’s finance payments and permitted under the applicable state lemon law. In many successful lemon law claims involving repeated warranty repairs, reimbursement of eligible finance charges may increase the consumer’s recovery beyond the payoff of the remaining loan principal.

However, interest is not always fully recoverable. If the loan includes negative equity from a prior trade-in or financing for optional add-on products, the manufacturer may argue that the related interest should not be included in the refund because those amounts are not directly attributable to the defective vehicle.

Common reimbursement and exclusion issues

A buyback scenario can involve several categories of money:

- Payments made toward principal and interest on the car loan

- Current loan balance and lender payoff

- Registration, taxes, and official fees

- Out-of-pocket expenses for towing, rental cars, or diagnostics

- Optional products such as GAP Insurance, service contracts, or maintenance plans

- Lease payments and obligations under lease agreements

- Prior negative equity rolled into the purchase

A manufacturer may agree to manufacturer reimbursement for some finance charges but classify others as excluded costs. The dispute often turns on statutory language, settlement negotiation, and documentation. Firms such as McMillan Law Group, led by Julian McMillan, and other consumer firms such as

Consumers in Southern California may also consult a lemon law attorney san diego for localized guidance, while statewide claims may warrant speaking with a california lemon law lawyer. For motorhomes and recreational vehicles, a specialized rv lemon law attorney may be appropriate because RV financing, warranties, and repair histories can be more complex.

How Mileage Offsets, Fees, and Payoff Amounts Affect Your Recovery

The mileage offset can significantly reduce the amount a consumer receives in a manufacturer buyback because it accounts for the vehicle’s use before the first qualifying repair attempt. A large usage deduction may reduce the refund enough that it no longer covers the remaining loan payoff, potentially leaving the consumer with negative equity unless the manufacturer agrees to pay the difference.

Consumers should also review settlement terms carefully when a replacement vehicle is offered. A replacement does not automatically eliminate the existing loan or lease obligations and may involve new financing, taxes, registration costs, or other fees. Confirming how the loan payoff, lease balance, and any remaining financial obligations will be handled is essential before accepting the settlement.

Practical Steps for Documenting Auto Loan Interest and Protecting Your Settlement

To protect your lemon law recovery in Rancho Palos Verdes, organize your financial records before settlement negotiations begin. Strong documentation makes it easier to prove the interest you’ve paid, identify any negative equity, and challenge an incomplete refund calculation, helping ensure you receive the full compensation you may be entitled to under the law.

Start by collecting:

- The purchase contract or lease agreement

2. The complete car loan payment history

3. Current payoff statement from the finance company

4. Records of all repair attempts and repair orders

5. Warranty documents from the manufacturer and warranty provider

6. Receipts for out-of-pocket expenses

7. Documents for GAP insurance, service contracts, and other add-ons

8. Any communications with the dealer, manufacturer, lender, or insurance company

Information found on Google, YouTube, Facebook, LinkedIn, X (Twitter), WhatsApp, or Pinterest can provide general background but should not replace legal advice for your specific lemon law claim. A free consultation with a qualified lemon law attorney can help determine whether interest is recoverable, whether the manufacturer buyback properly addresses your loan balance, and whether a replacement vehicle or cash refund is the better option.

Before signing a release, confirm the settlement states who pays the lender, when the payoff will be made, whether per diem interest is included, and whether the loan balance will be fully satisfied. Also verify how the settlement treats usage deduction, negative equity, interest paid, optional add-ons, and any remaining obligations that could affect your rights, credit score, or future financing.